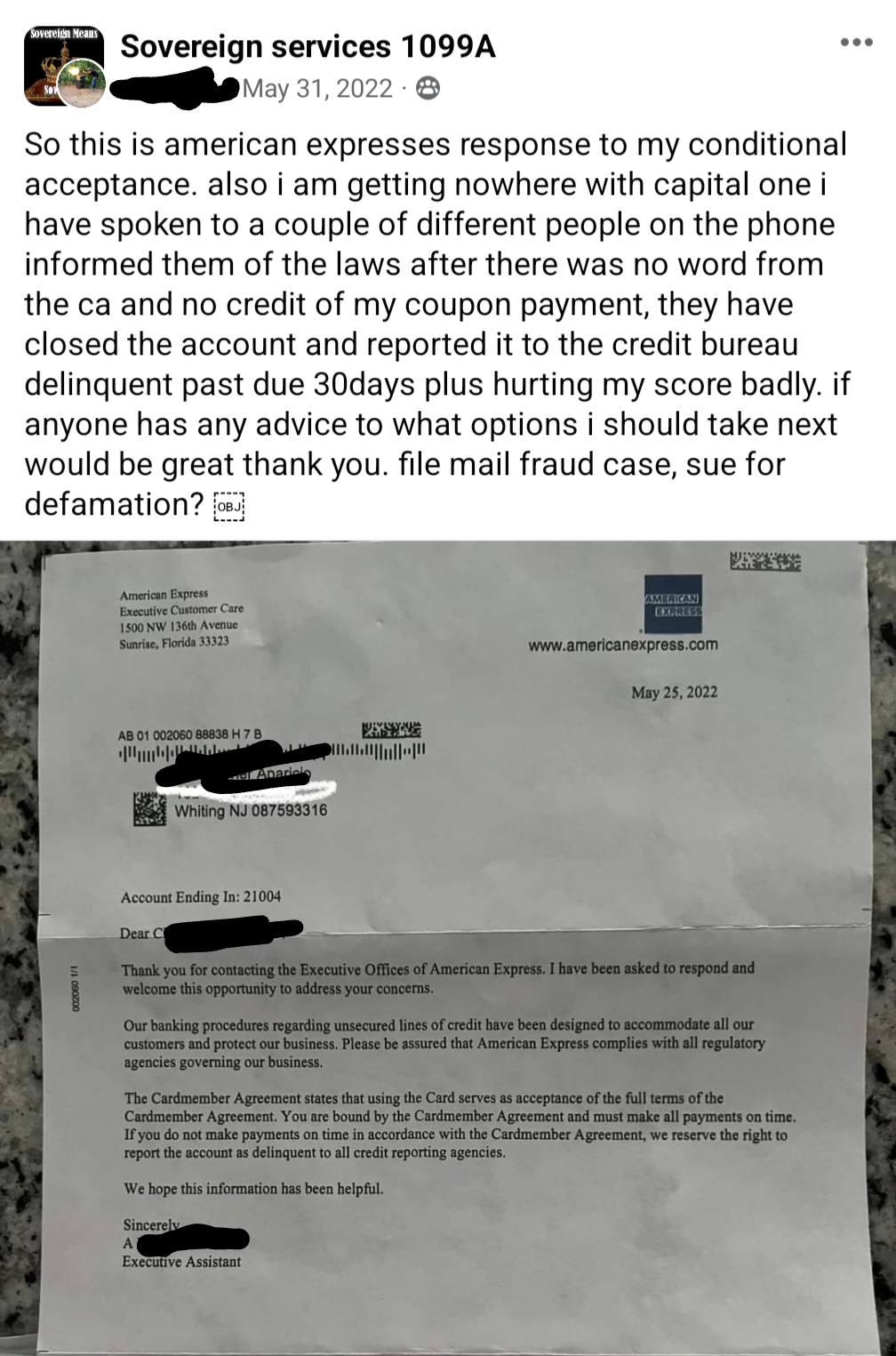

I will grant one thing: the whole “the card agreement says that using the card counts as accepting the agreement” is circular logic like “the Bible is true because it says it’s true”. There should be an obligation to get that agreement before any card is issued. Using a card shouldn’t cancel out any requirement of informed consent. These people clearly don’t have a good understanding about how any of this works, even if they are trying to abuse these things in the way they understand them.

Like there were aspects of my credit cards, that I was using in good faith, that I didn’t really understand until years after I’d been using them.

I’m not sure if it’s different in the states, but in the UK it’s definitely like that.

You sign the agreement, the card is dispatched.

The card arrives with more literature, and it is made very clear that by using the card you accept the terms.

If you decide that you don’t like the terms, you can return it un-used, or even I believe within 14 days you can cancel everything and just pay off any money you’ve spent with it.

Correct. As well as literature and mandatory language detailing how to report fraud, or complain to a specific governing agency if you believe the card issuer is treating you unfairly or not complying with applicable laws. In the US, that would likely be the CFPB (Consumer Financial Protection Bureau).

It is not circular logic. It’s closer to “you’ve agreed to the terms of the Bible because you used the Bible for your benefit.” Still not quite the same as the credit card agreement, but closer. Clearly not circular.

{kind=link}

I will grant one thing: the whole “the card agreement says that using the card counts as accepting the agreement” is circular logic like “the Bible is true because it says it’s true”. There should be an obligation to get that agreement before any card is issued. Using a card shouldn’t cancel out any requirement of informed consent. These people clearly don’t have a good understanding about how any of this works, even if they are trying to abuse these things in the way they understand them.

Like there were aspects of my credit cards, that I was using in good faith, that I didn’t really understand until years after I’d been using them.

I’m not sure if it’s different in the states, but in the UK it’s definitely like that.

You sign the agreement, the card is dispatched.

The card arrives with more literature, and it is made very clear that by using the card you accept the terms.

If you decide that you don’t like the terms, you can return it un-used, or even I believe within 14 days you can cancel everything and just pay off any money you’ve spent with it.

It’s the same in the US. Most people don’t bother reading any of the terms, so they’re surprised when they exist.

There’s often things that beneficial to the user in those terms too. Buyer protections, terms with specific vendor types, etc.

Correct. As well as literature and mandatory language detailing how to report fraud, or complain to a specific governing agency if you believe the card issuer is treating you unfairly or not complying with applicable laws. In the US, that would likely be the CFPB (Consumer Financial Protection Bureau).

You do get a copy of the card agreement before a card is issued. Banks are pretty tightly regulated in this area.

Note that is not always the case, which is why car makers can surveil you simply for riding in the car. Being in the car constitutes acceptance.

It is not circular logic. It’s closer to “you’ve agreed to the terms of the Bible because you used the Bible for your benefit.” Still not quite the same as the credit card agreement, but closer. Clearly not circular.